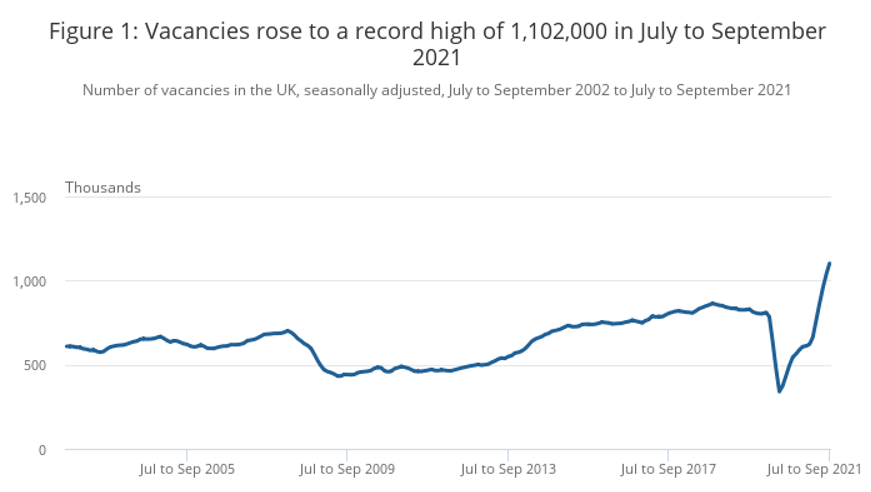

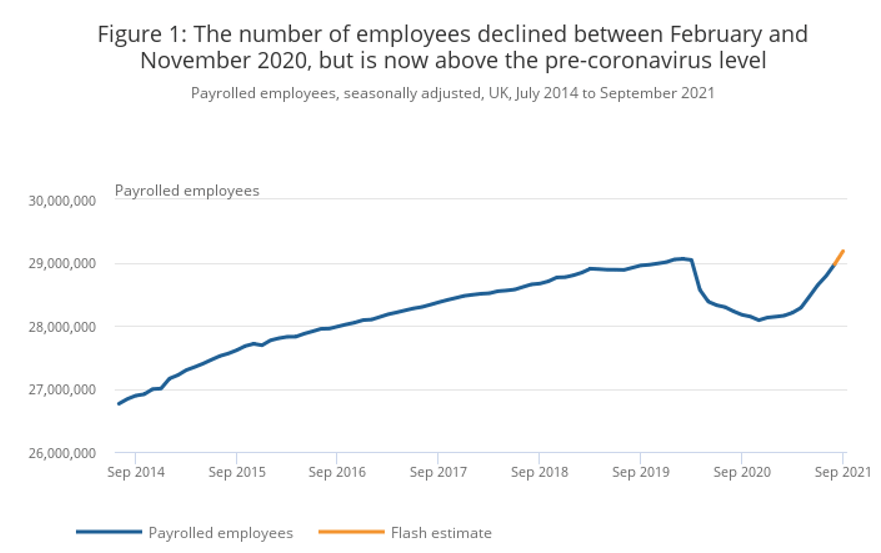

The Bank of England has always suggested that employment would get back to normal by the end of this financial year. But it looks like we are going to get there a lot quicker.

For employers, this means that there are just fewer people to choose from at the moment and what’s more, candidates have a lot more choice given the record number of vacancies.

Furthermore, The Bank of England predicts that unemployment is likely to keep decreasing until 2024, so talent pools will only continue to shrink.

So, what should employers consider doing in such a competitive market? Here are six things you can do right now:

1. Don’t wait. Hire the talent you need now. Wage inflation is likely to remain at high levels. It is currently at 7.2% (June to August 2021) and to put that into context, pre-covid it was at 2.2%. If you need someone, hire them now – talent pools are decreasing so it is only going to get more expensive to recruit. The quicker you can move, the higher chance you have of landing a candidate interviewing with you. If your recruiting process moves slowly, you will have other companies’ job offers undercutting yours. A candidate may rank your opportunity the highest, but between a 50% chance of landing yours and a 100% of landing another good option, most will go for the safe bet.

2. Keep up with salary inflation. Are you offering the right level of pay to existing staff? Is it enough to retain the key skills you need? Are you offering the right level of pay for your new roles? Reach out to your Stanton House contact for help with your salary benchmarking.

3. Stay organised.

Try and make the candidate journey as slick as possible. A disorganised process

will make you look like a disorganised company. Missed scheduling emails,

incorrect Zoom links, slow feedback – any one of these can sink all the

work you put into interviewing so far.

4. Assess the skills and competencies you require. Be more flexible on what you consider to be the essential versus desirable skills and competencies for each role. Can you reshape a role / broaden responsibilities to make it more attractive to a wider pool of talent? Reach out to your Stanton House contact so we can get ahead of the curve and start building the talent pools your team needs to grow.

5. Evolve, articulate and promote your Employer Value Proposition (EVP). What is it about you that is different? What makes you stand out as an employer of choice? Why should people want to come and work for you? Are you a diverse and inclusive employer? Are you committed to flexible working, and how do you prioritise the mental wellbeing of your employees?

6. Offer remote & flexible working. You will struggle to hire candidates if you require them to

be in the office all of the time. Flexible and remote/hybrid working is taken as a given these days!

.png)